In markets where the investment ecosystem is still underdeveloped, which means many countries in Europe, it’s often said that a sign of maturation is the amount of capital that companies attract from international investors.

In the case of Spain, there are two main reasons behind this:

International VCs provide the necessary capital and connections for startups to expand and grow.

Early stage capital is abundant but there are only a handful of firms able to invest in €5+ million rounds.

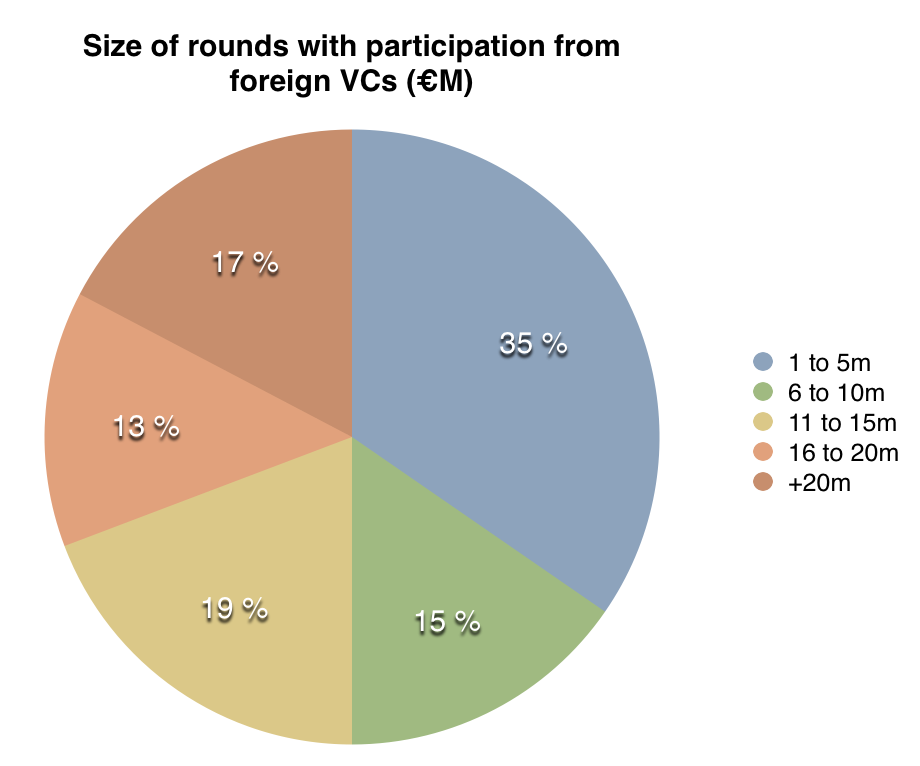

With still a few days to go in 2015, the record has been broken once again, with at least 44 international investment firms participating in Spanish deals this year.

Unsurprisingly, foreign VC firms participated in all but one large deal that took place in Spain (Jobandtalent’s €23 million round), once again showing that when companies need a lot of capital, international investors are the ones who provide it.

Worth noting is also the fact that these investors not only provide growth or venture money, but are also increasingly investing at earlier stages. As the following chart shows, 35% of all foreign VCs that backed a Spanish company in 2015 invested in rounds smaller than €5 million.

Typeform was one of the first Spanish companies to have only raised capital from non-Spanish investors, but we’re quickly seeing an increase in the number of startups that, after FFF and pre-seed rounds, tend to only raise internationally. Kompyte, Stampery, Monkimun, Verse, Winko Games, Novicap or Medtep are examples of this.

In terms of the most active foreign investors, Accel Partners, Nazca Ventures, Eight Roads (Fidelity Growth Partners Europe) and Partech Ventures all participated in more than one deal in 2015.

In order to help other startups and the overall Spanish community in the process of identifying these funds, I’ve put together the following Google spreadsheet which includes a list of the international investors, their location, the startup they backed and size of the deal they participated in.

(This post was written by Javier Escribano, former co-founder of TouristEye and Selltag, and originally published on Medium. Javier is currently seeking a VP of Product, CTO or PM role. You can check his LinkedIn profile or contact him if interested)

I have raised 3 rounds of seed investment (~700k€ in total), no Series A yet; so my advice is limited by that experience. However, it’s consistent with the experience of other founders with more experience I talked with.

The key learnings on this article are:

Plan your investment process with a board in Trello

Always find an intro

The pitch must be a conversation, not a monologue

Build three different decks, one for each stage of the process

Use Demo Days to strengthen the company brand

Plan your investment process with a board in Trello

I recommend you to have a Trello board for each round of investment. Add all the investors you want to talk to and then, move them through this funnel:

Discarded: Investors who have rejected you or you have discarded (they have invested in a competitor for example).

To contact later: Investors who are interested but need to see more months of data.

Intro to be found: You need to find someone who knows the investor.

We have an intro: You know someone who can make an intro.

1st contact: You have talked with them once.

2nd contact: You have talked with them twice or more.

Want to invest: Investors who want to invest.

You should add the main information of the investor in the description of each card (range of investments, total investment per company, companies invested, people you know who can make an intro). Each time you have an interaction with them, add a comment on the card with their feedback or your impressions. That way, your co-founders can see the evolution and you don’t need to keep forwarding emails.

Always find an intro

I’m sure you have already read this tip in many places, so consider it another reminder that it does work way better to have an intro than to send a cold email or call.

Sometimes is hard to find someone who knows the investor, but you can always find a way. Of course, you can use LinkedIn; although be careful because lots of connections are really poor links. Before asking someone to make you an intro, ask him/her how good do they know the investor. Not all intros are worth the same

Another way is to meet someone who knows the investor; and the best people are probably the founders/CEOs of the companies he/has invested in. You should ask someone you know for an intro to that founder (a cold email/tweet may work too), ask him/her for advice on investment/roadmap over coffee and then ask him/her if he/she thinks his/her investor is a good match for you. If he/she thinks so, there you have a good intro!

The pitch must be a conversation, not a monologue

This is a typical mistake we do when we talk to investors. We try to communicate everything, assuring the investor we know everything about our business, we have a clear roadmap and we are the best team to achieve it.

However, it’s not the best way to convince an investor. You have to make him/her engage with you intellectually, you want him/her to ask you questions you know the answer, you want him/her to get into the problem you are solving really deeply so he/she keeps thinking about it for the next days.

If it’s a monologue, he/she will not remember. If you make him/her think about it and engage with the problem; you will in a better position to convince him/her. Take into account that when you are talking to an investor, your competitors aren’t the company competitors but other startups which are also raising and talking with him/her. The investor can only invest in a few per year, and he/she will end up comparing deals.

Build three different decks, one for each stage of the process

I recommend you to have 3 different decks:

Intro deck

This is the deck you will send over email to an investor to check if he/she is interested. It should have 10–12 slides, with key information about the team, problem, key parts of the solution and your metrics. Slides should be simple, with 1–3 phrases per slide; the investor will glance over them to see if it’s worth spending time on you.

Examples of slides with just one phrase.

Meeting deck

There are investors who prefer to talk on the meeting instead of following the script of your deck; and there are others who prefer to follow the deck and then ask you questions.

In both cases you will need a deck with much more information that the Intro deck but removing the phrases you are going to say. Remember they should look at you 80% of the time, not to the slides.

Examples of slides with just one phrase.

If you follow the deck on the meeting, you shouldn’t show all the slides. Leave many of them at the end, specially the ones which dig deeply into a topic (user acquisition, patents, tech…). If the investor asks about it, you have the slide. You will earn two points: one for being brief on the pitch and another for having the information prepared.

After meeting deck

Investors will ask you for the Meeting deck. You can’t send it because it doesn’t have the key phrases you said. You need to add those key phrases into the deck and reorganize it a bit so it follows a logical order (no just-in-case slides at the end).

Extra: Demo Day deck

This deck is like the Meeting deck but with just the slides you are going to pitch. You may need to remove text from it to make sure everyone looks at you 80% of the time (if people read the slide instead of listening to you, you have failed as a presenter).

We can summarize them:

Use Demo Days to strengthen the company brand

Don’t think Demo Days or public pitches will bring you an investor just after the pitch. It doesn’t happen. The only place I’ve personally seen it was in a 500 Startup Demo Day in Silicon Valley, when a founder of another startup received a text just after finishing her pitch saying he wanted to close the round with $100k. But the truth is that she had already talked him over email. I’m sure there will cases, but they are just 0.01%.

What you need to do in those pitches is strengthen the company brand so investors and potential new employees remember your company later; andmake sure everyone who listen will agree that you seem to be a trustworthy and reliable CEO. If you do, they will be more predisposed to meet with you even if it’s a cold email or call.

Enjoy the show and have fun, but don’t worry too much. The best startups almost never were the best ones in Demo Days anyway.

Plug and Play Spain, the Valencia-based branch of the Silicon Valley accelerator, has just announced the launch of a fintech program with the participation of Banco Santander.

The program, which is currently accepting applications, will start in February 2016 and is aimed at financial technology companies at different stages of development. “We’re not necessarily looking for early stage startups that need to be accelerated”, Plug and Play’s Juan Luis Hortelano told me. “The idea is that the startups selected can take advantage of the Santander connection and also of PnP’s Silicon Valley demo day”.

This is not the first fintech vertical launched by the US accelerator. In previous occasions it has partnered with Deutsche Bank, Citi or Capital One for similar programs. Santander was already a partner of Plug and Play in the US.

The fintech startups chosen by Plug and Play Spain will coexist with the rest of the companies in the batch, but will be able to attend specific mentoring sessions and workshops from industry personnel. The companies will stay in Valencia throughout the program -which lasts 4 months- and will also be allowed to stay at Santander’s offices in Madrid.

In a statement, Plug and Play says that “chosen projects will be eligible to receive funding from PnP and participate in pilot programs with Santander”. Asked about this, Hortelano told me that their intention is to “financially support participating fintech startups that are at a pre-seed or seed stage”. With more mature companies, the accelerator is open to negotiating specific terms and conditions. “For example, advisory shares for those that are mature if we can help them in their US expansion or to find the right partners”, he said.

Santander, in theory, won’t invest in the companies.

Banco Santander’s startup investments

As head of Santander UK, Ana Patricia Botín launched Santander InnoVentures, a London-based $100 million fund to invest in fintech startups. So far, the bank has invested in iZettle, Cyanogen, MyCheck, Ripple and Kabbage.

Following the death of his father, Ana Patricia Botín took over the global institution and has pushed hard to install a digital-first mentality in the bank.

“I think of digital as a means to an end: How do I service and get more loyal customers: how do I achieve operational excellence and how do I change my culture?”, she recently said in an interview with the Financial Times. “Those are my three building blocks and if you think about it, digital comes into it in every single one of them.”

Ms Botín also said that she considers Apple, Facebook, Google and Amazon as the companies that pose a bigger threat to the bank’s business. “These big four guys, they are worth more than us, they have more cash and they have less regulation”.

Kibo Ventures is about to launch a new fund. If all goes according to plan, the fund will be almost double the size of the first one (€80 million vs. €45 million), allowing the firm to lead or co-lead investments in the €2 to €5 million range.

Not a lot of investment firms can reach that level in Spain at the moment, and with so much seed capital available for startups, the firm led by Aquilino Peña, Javier Torremocha and José María Amusátegui believes they can make a difference at the Series A and B stage.

To know more about the firm’s intentions, the differences between the new and old fund and LPs’ appetite for technology companies, we sat down with Aquilino Peña for a short interview.

You’ve significantly increased the size of this new fund, from €45 to €80 million. What’s going to change with it? Is Kibo’s focus different this time?

The focus is the same as before: to invest in digital companies. We don’t invest in hardware, retail, consumer electronics or in other capital-intensive sectors that require large sums of money to launch a product or service. In digital we’ve made deals in all kinds of sectors, mostly because the Spanish market doesn’t allow you, as an investor, to focus on a niche or single sector.

We’re big fans of transactional models (SaaS, ecommerce enablers, marketplaces), mobile and companies with a strong tech component.

Can you find enough projects in Spain to justify spending €80 million in them? In other words, are you going to continue to invest only in Spanish companies or are you also looking at other countries and regions?

One third of the 31 companies in our portfolio are in the US, so we don’t only look at Spain-based companies. That said, the common trait in our portfolio is that there’s always a Spanish connection: the founding team, the development team, etc.

We do make deals outside of Spain under that thesis, but only when we can contribute to their success in some way and when there’s a Spanish link in them. Many of the companies we have backed have launched in the US with our support, and we like to help in any way we can.

You’ve always said that, with so much capital at the seed stage in Spain, there’s a big opportunity for firms investing in large Series A and B rounds. Is that Kibo’s goal with this new €80 million fund?

Our average investment in our current fund is €1 million. With the new one, we want to invest in fewer companies but with the capability of deploying more capital than before in each of them, between €3 and €4 million per company.

With the new fund we’ll have the same entry point, but we want to be able to lead or co-lead €2 to €5 million rounds in Spanish companies. Right now it’s very tough for startups to find local money at that stage and the fundraising process tends to be an even bigger distraction for teams.

We’re hands-on investors, we believe we know very well our companies and that’s why we want to lead those type of deals, instead of just making small follow-on investments.

VCs don’t talk much about their own investors. Who is backing Kibo this time? Are Telefonica with Amérigo or Mutua Madrileña investing once again?

We’re right in the middle of the fundraising process and all LPs from our first fund have encouraged us to launch the second one, and they have backed us. Pretty much every single one of them have already committed capital to the new fund, and those that have not, are currently discussing it internally. Our objetive is that all of our previous investors join us once again, and it’s looking good.

We’re very happy with Telefonica’s Amerigo, and we collaborate with the company at all levels: sales agreements, co-investments, analysis of opportunities and support in their various entrepreneurship programs under the Open Future umbrella.

There are a lot of funds raising capital at the moment. I think LPs are very selective when it comes to backing VCs, and not every single fund currently fundraising will be able to reach their goals. You need to have experience, strong differentiating factors and a strategy and focus that you can explain well.

In our case, we have all of that and we also have the support of our previous LPs. The process is going very well for us.

People often talk about how tough it is for a startup to raise funding. But, what’s the process like for a fund like Kibo? Is there a lot of interest from LPs to get into the technology market?

The problem we have in Spain is that the number of institutional investors willing to invest in Venture Capital is very limited. That’s one of the reasons why companies like Telefonica or public entities such as FondICO or CDTI’s Innvierte play such a vital role in the sector.

“In Spain the number of institutional investors willing to invest in Venture Capital is very limited” – Aquilino Peña

This problem is slowly but surely being solved, mostly thanks to companies that are performing well and growing, coupled with significant exits and low interest rates.

What many LPs and institutional investors now realise is that they’re better off investing in Venture Capital firms with strong track records than investing that capital themselves.

You told me that the new fund will have a size of between €60 to €80 million. Does its final size depend on how much public money you’re able to get?

We’re the only fund in Spain that, so far, has received support from FondICO and CDTI in both of our funds, the old one and the new one.

We’re also in talks with the EIF (European Investment Fund), which is the largest institutional investor in the European Venture Capital scene, managed by people with a lot of experience in the sector. We’ll be happy to have them on board, but they’re not investors yet.

What are you most proud of in your first fund?

One of the key advantages of our portfolio is that we don’t depend on one or two companies to perform well. We’ve been able to build a portfolio that has seen very few casualties.

We’ve invested in 31 companies, we’ve sold profitably three of those, four have shut down (less than 5% of all) and two more are currently struggling.

All in all, we have a very solid and growing portfolio, with aggregate annual sales of €50 million and with more than 800 employees. These are companies that have found their market and have real clients. Thanks to our efforts to stay connected in the ecosystem, we’ve been able to invest in some of the better companies in Spain today. Some of the most valuable in our portfolio are Flywire (peerTransfer), CartoDB, Redbooth or Jobandtalent; but we’re also investors in others that have great potential, Captio, iContainers, Custodio or MediaSmart.

These days, on the consumer side, it seems as if two main kind of apps are the most lucrative: games and dating applications. If you take a look at the top grossing apps on iOS or Android’s app stores, you’ll see a wide variety of the latter, from Tinder to Happn. Groopify wants to get there.

The Madrid-based startup is not just a dating app, but also a platform that makes it easier for groups of young people who don’t know each other to meet up for a drink. Like a blind date, but more sophisticated and with more people involved.

According to Pablo Viguera, co-founder and CEO, in 18 months the app has more than 100,000 registered users and the number of businesses that have partnered with the app has surpassed the thousand mark.

As Groopify brings new customers to bars and cafés, the company believes it can monetise that relationship to build a sustainable business model.

“We don’t only provide recurrent and quality traffic to bars thanks to our meetings, but we also help them in their communication and marketing efforts”, the company says. Groopify charges a pay per lead commission to bars. The company is not publicly saying how well that business model is working, nor will it disclose sales or revenue figures.

Viguera did say in a statement that in the last 12 months the number of plans created by users has grown 10X, and that 2,000 plans are created on a monthly basis in 45 different Spanish cities.

To expand its presence and start rolling Groopify internationally, the startup has just closed a €800,000 round of funding led by media for equity investment firm Media Digital Ventures (Atresmedia, Godó, Vocento), Pinama Inversiones and business angel José María Torroja (through a Startupxplore syndicate).

Groopify had previously raised €180,000 from Plug and Play Spain, Grupo Zriser, Civeta and Carlos Domingo.

Example of the 8 Spanish entrepreneurs educated at MIT and global leaders in their fields.

This guest post was written by Iñaki Berenguer, currently the founder & CEO of CoverWallet. Prior to that, Iñaki founded and led Contactive and Pixable (both acquired), and worked at McKinsey, Microsoft and HP.

This summer, Nobel prize winnerPaul Krugman published anarticle in the New York Times about the dominance of MIT trained economists in global policy positions. He gave as examples, apart from himself,Ben Bernanke,Mario Draghi,Olivier Blanchard orMaurice Obstfeld, Chief Economists of the IMF, European Central Bank, or Federal Reserve. Morerecently, a new ranking puts MIT as the top ranked university worldwide. And this very week, MIT published astudy about the impact of the university in the creation of businesses, that in turn generate employment for 5 million people and enough income to be ranked as the 10th largest economy in the world in terms of GDP.

It’s very remarkable that a university that accepts only 1,100 students in its freshmen class has graduates with that level of impact. Not only in Economic Policies, but also with the global establishment, with individuals likeBenjamin Netanyahu,Carly Fiorina,Kofi Annan,John S. Reed (President of Citigroup), orWilliam Clay Ford (CEO of Ford), as well as in the creation of technology companies like Dropbox, Texas Instruments, Intel, HP, Analog Devices, Akamai, Qualcomm, Bose, Genentech and Koch, 80 Nobel prizes (Spain has only 8), and visionaries such asSir Tim Berners Lee orNoah Chomsky.

MIT and the Spanish startup ecosystem

But the really remarkable thing is the impact of MIT in Spain. For example, less than 10 students each year get accepted into MIT Sloan. Even so, this has an interminable representation in the Spanish establishment. Some of those who graduated MIT includeCarlos Torres (President of BBVA),Rafael del Pino (President of Ferrovial),Tomás Pascual(President of Leche Pascual), Matías Rodríguez Iniciarte (Vice Chairman of Santander Bank),Joaquin Moya (President of IBM Spain),Miguel Milano (President of Oracle Spain and Salesforce),Enrique Casanueva (President of JPMorgan Spain), Nuria Oliver (Scientific Director of Telefonica),Fernando Perez-Hickman (Chairman Sabadell Bank), orMaria Teresa Pulido (Board member of Bankinter), as well as a number of partners at McKinsey, BCG, Bain or ATKearney.

But I wanted to talk about the impact of MIT in Spain, and specifically, in the innovation and creation of startups with global impact. I’ve chosen 8 prominent examples of Spanish entrepreneurs educated at MIT (just like me) whose startups are worldwide referents in their fields:

Iker Marcaide, founder of peerTransfer (Flywire) in 2009, world leader in international payments. The startup has received more than $40 million in funding from investors like Bain Capital o Accel (Facebook investors), and has processed transactions worth of +$2bn.

Jose Mariano López Urdiales, founder of Bloostar, a pioneer company in the launching of nanosatellites. Also included in his team isMichael Lopez-Alegría, a Spanish astronaut that maintains NASA’s world record for most days in space.Here you have a video of their launch.

Bernat Ollé, founder of PureTech Ventures and founder of Vedanta Biosciences, that develops pharmaceuticals from bacteria and that recently signed a $250MM agreement with Johnson&Johnson.

Javier García Martínez, founder of Rive Technology, which develops nanomaterials to maximize the performance of catalyzers used in the refining of oil and has received $80 million in funding.

Angel Diaz Alegre, founder of iDoctus, a tool of mHealth for doctors.

In the last few years, many groups of Spanish tech innovators are emerging with global ambition (apart from the ones mentioned, there are many more like JobandTalent, Wallapop, Ticketbis, Typeform, CartoDB or AlienVault) that have become global referents in their industries, something that was unthinkable 10 years ago.

A decade ago, the path was to grow first in Spain and after a number of years, get out into the world, which in the majority of cases did not end up happening. This is changing and the representation of MIT for this type of global founders is really formidable.

The MIT gang

What distinguishes MIT and what makes it so innovative? Its DNA and the entrepreneurial culture.

MIT was created almost two centuries ago with the motto “Mens et manus” (Mind and Hand) to give technological service to the needs of the industrial era. And as the world was changing at a dizzying speed, in recent years MIT has also transformed into an incubator of leaders in the digital era. Leaders that are prepared to face the challenges of modern society and take advantage of opportunities that this changing world presents with the support of new technologies.

“For innovation-driven startups, the ability to enter and potentially disrupt a market requires not only innovative ideas, but also productive workers to commercialize and execute those ideas”, Professor Ed Roberts.

The whole university breathes the passion to innovate, and its DNA, coupled with its capacity to bring together the most brilliant minds on the planet, becomes an explosive combination.

This, when added to an ecosystem of investors, advisors, professors that have founded companies, mentors, funding, coworking spaces, state-of-the-art research, a multitude of classes about entrepreneurship, offices of assistance for those starting out, labs of large technological companies (e.g., Microsoft, Google, Facebook, etc) located in the same campus, and daily networking opportunities, prepares you to create companies that change the world using new technologies.

I started Novobrief because I thought, and I still do, that the Spanish startup ecosystem could be covered in a better way and because I believed investors, entrepreneurs, corporates and the general public outside of Spain should know what was going on in the country.

The idea behind the project was always to build a business that could support myself, but I haven’t been able to achieve that and, in the process, I’ve also learned that simply covering Spain is too low of a ceiling.

A few months ago I started working on a database of Spanish startups with Javier Escribano. We both believed that building a database of such characteristics could be useful for local startups, entrepreneurs and investors. And also, it could represent a new source of income for myself and the blog.

Also around then, I had another conversation with Robin Wauters, whom I have known and respected for many years. We talked about what he had in mind for Tech.eu and it all sounded very familiar with the way I saw things for the future of Novobrief, but with Europe (and not just Spain) as a starting point.

Several conversations later, we agreed that I’d join Tech.eu as a data analyst/journalist. I’m starting this week.

I’m super excited about the opportunity and what I’ll be doing in the near future. I won’t be publicly publishing a lot of stories anymore, but I’m sure I’ll learn ten times as much.

Novobrief won’t go away and nor will the newsletter.

It’s taken me a lot of time and hard effort to build this, and I don’t want it to disappear. Obviously, I won’t be publishing as much as before and this will become more of a personal publication focused on the Spanish startup scene. But I will continue to do so from time to time, and I might even publish a few articles in Spanish.

Por primera vez en la historia de España, en 2015 se invirtieron más de 500 millones de euros en empresas tecnológicas españolas. Lo que viene a ser en la mitología estartapil, un medio unicornio.

Sin más datos en la mano, es difícil afirmar que 2015 ha sido un año record en otros aspectos del panorama patrio de startups. Sin embargo, y ayudado en mi mala memoria, creo que no me cojo los dedos si digo que el año pasado fue también especialmente bueno para los inversores españoles.

No porque se invirtiera más dinero que nunca en empresas españolas, sino porque los propios fondos de capital riesgo locales y otras sociedades de inversión levantaron cantidades ingentes de capital que ahora tendrán que determinar en qué empresas meter.

Mientras que en 2014 los tres principales fondos de inversión que se cerraron fueron los de Axon, Caixa Capital Risc y Cabiedes & Partners, sumando casi 100 millones de euros, en 2015 la lista es mucho mayor.

Qualitas anunció a mediados de año un fondo de 60 millones para invertir en etapas maduras. Después de años de sequía, Nauta Capital hizo lo mismo y parece que van encaminados a cerrar su nuevo fondo en 150 millones de euros. Hotusa Ventures hizo lo propio con un vehículo especializado en el sector del turismo. Carlos Blanco parece que va a montar un fondo de early stage de 20 millones. Dice la leyenda que Javier Santiso está a vueltas con el suyo de growth, pero que le está costando más de lo previsto cerrarlo. Lánzame Capital prepara 20 millones para principios de este año, elevando su anterior pledge fund a la enésima potencia. Samaipata Ventures apareció a finales de 2015 con 20 millones bajo el brazo para empresas de ecommerce, apoyados en la multimillonaria venta de La Nevera Roja. Kibo Ventures cerró el año afirmando que Papá Noel ha bajado este año por la chimenea con un cheque de 80 millones. Galdana Ventures tiene 150 millones en la saca para invertir en otros fondos. Y, esto todo, sin contar con el nuevo fondo que K Fund (Vitamina K, Iñaki Arrola) espera cerrar pronto y que andará entre los 40 y los 50 millones.

En total, y si se confirman los que quedan por cerrar, hablamos de en torno a 550 millones de euros que están esperando ser invertidos en empresas tecnológicas.

Por poner estas cifras de fundraising en contexto: entre 2015 y los primeros meses de 2016 es muy probable que el dinero levantado por los fondos… sea superior al invertido en todo 2015. Y 2015 fue un año record.

O dicho de otra forma, entre 10 y 15 fondos de capital riesgo españoles tienen en sus manos una cantidad de dinero lista para ser invertida… superior a la suma de todo lo invertido en 2013 y 2014 (221 y 285 millones, respectivamente).

Resulta un tanto curioso que después, algunos fondos, se echen las manos a la cabeza con las valoraciones de algunas startups early stage. ¡Burbuja! No recuerdo muchas cosas de la carrera, pero sí recuerdo que una de las primeras cosas que te enseñan en macroeconomía es que a mayor cantidad de dinero en circulación en el mercado, mayores precios.

El ‘montemos una startup, que está de moda’ parece que se ha convertido este año en el ‘montemos un fondo, que hay pasta de sobra’. Y hay mucho dinero por dos principales motivos: porque el Estado, a través del ICO, está subvencionando el sector con 1.500 millones de euros para los fondos y porque mucho inversor no tecnológico se está acercando a la tecnología como un niño se acerca al mando de la Play el día de Reyes.

Visto el panorama cabe preguntarse en dónde se va a invertir todo este dinero.

Según las cifras que he ido recogiendo para Novobrief estos últimos años, de 2013 a 2015 la cantidad invertida en startups españolas se incrementó un 142%. Sin embargo, el número de operaciones (dicho de otra forma, la cantidad de startups listas para recibir inversión), tan solo un 23%.

Con más cantidad de dinero disponible que nunca en el mercado, ¿a dónde va a ir a parar? Uno podría pensar que los fondos españoles comenzarán a invertir fuera de España, pero más allá de Nauta Capital, Axon, Active VP y Seaya Ventures, pocos lo han hecho en los últimos años. En parte, me imagino, porque el deal-flow de mucho inversor español más allá de nuestras fronteras es tan bueno como la calidad del aire de Madrid.

Cabiedes & Partners, un clásico de la inversión patria, decía en 2014 que con el nuevo fondo comenzarían a invertir fuera de España. Como se suele decir en interné, ‘photo or didn’t happen’, y por ahora parece que es más lo segundo.

Todo esto, sobre todo la (no) exposición internacional de los fondos españoles, ocurre en un momento en el que cada vez más fondos de UK, Francia o Alemania nacen con un enfoque pan-europeo desde el día uno.

Si el mercado objetivo para la mayoría de fondos españoles empieza en Tarifa y acaba en los Pirineos. ¿A dónde carallo van a ir a parar todos esos millones de euros que están esperando para ser invertidos?

Today was the official unveiling of the 2016 edition of 4YFN, one of the leading startup and technology events in Spain. Organised by Mobile World Capital, the conference will take place in Barcelona from February 22 to 25 and will bring together 12,000 attendees, 500 investors and startups from all over Europe.

For this year’s edition, MWC asked me to put together a report on the Spanish startup ecosystem, which you can see embedded above. The report was presented by MWC’s CEO Aleix Valls.

Disclaimer: this was paid work.

I think it’s a pretty good summary of what happened in Spain in 2015 and the main challenges the country still faces when it comes to building technology companies. One thing that I forgot to include in the report is the fact that in 2015 Spanish VC firms raised almost more capital than what was actually invested, which makes you wonder where all that money is going to go (over the next few years) and which will increase investor competition and push valuations higher.

PS: If you want a higher quality (images & graphs) version of the report, get in touch (jaime@novobrief.com) and I will send you one.

Just Eat is going to get its hands on the company once founded by Jose del Barrio and Iñigo Juantegui, becoming a de facto monopoly in the Spanish delivery industry with approximately 6 million annual deliveries.

While I understand that the transaction between Just Eat and Rocket Internet was closed very recently, the Berlin-based giant is waiting to complete the sale of other business units in its Global Online Takeaway Group to make an official announcement.

Global Online Takeaway Group is the name of the holding company Rocket created in February of last year when it acquired at least 7 food delivery companies in two different continents, including La Nevera Roja and Pizzabo (Italy). At the time, Rocket also announced a €496 million investment in Delivery Hero, one of the bigger companies in the sector and a competitor of FoodPanda.

Since its IPO in October 2014, Rocket’s stock price has dropped by more than 50% and currently trades at €18.80. At the time of the IPO, the German giant had a market cap of €8.4 billion. Rocket’s current market cap stands at €3.10 billion, still the most valued technology company in Europe.

Rocket has come under strong scrutiny by investors and the media in recent times. According to Reuters, the company decided at the last minute to put HelloFresh’s IPO plans on ice due to internal turmoil and significant differences with Kinnekiv, the Swedish investor firm that controls 14% of Rocket’s shares and is also a major investor in many of its subsidiaries.

On the other hand, UK-based Just Eat’s share price rose 40% over the past 12 months while orders increased by 57%.

In October 2015, the Financial Times wrote about “the German ecommerce group struggle for profitability”, citing numerous analysts and investors who have, for a long time, complained about Rocket Internet’s complexity. Rocket has lost a number of key senior managers over the past few months.

Co-founder Oliver Samwer talked about these and other issues at London TechCrunch Disrupt in an interview on stage.

According to my sources, Rocket is also planning significant layoffs at Linio, one of the largest online retail stores in Latin America. These sources say that 30% of Linio’s staff could be let go in the next few weeks. Linio currently has 1,500 employees across the region.

A 12-month acquisition

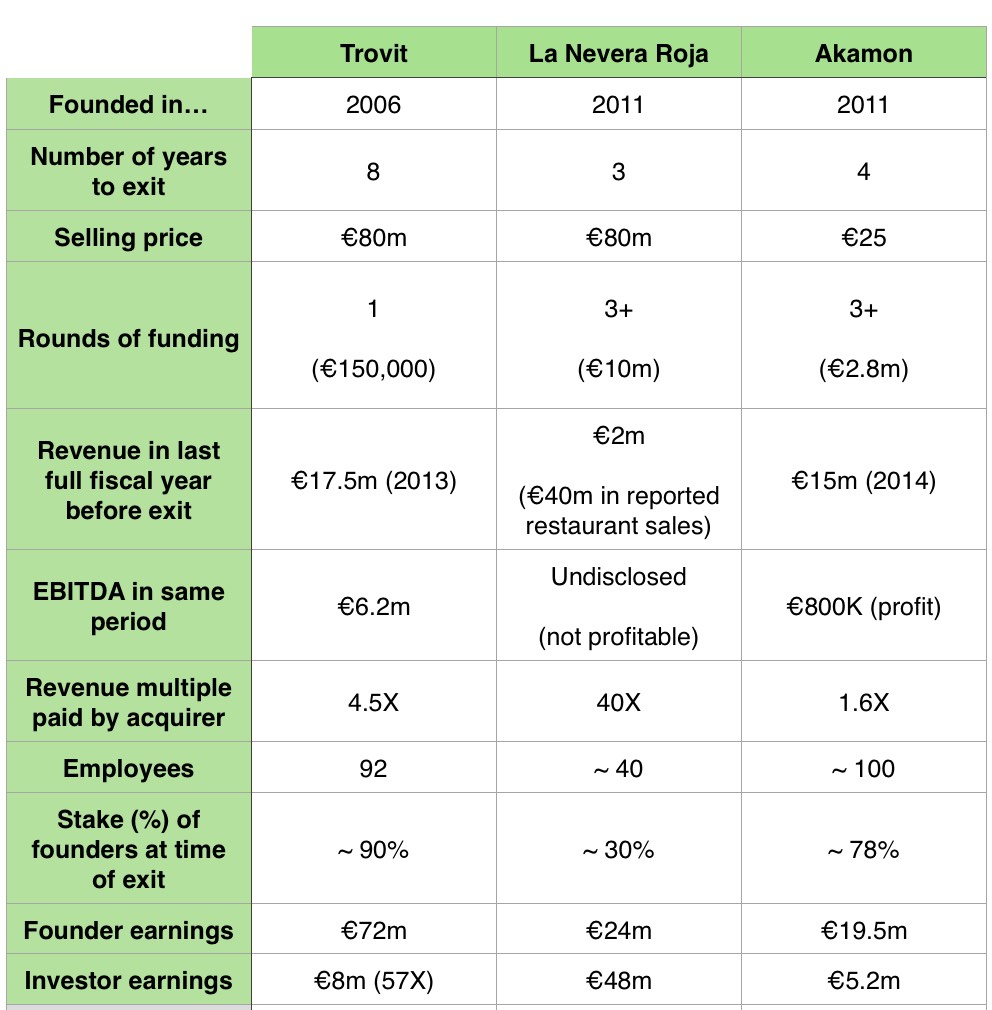

La Nevera Roja’s acquisition by Rocket Internet was the largest exit by a Spanish technology company in 2015, not counting Mitula’s IPO on the Australian Stock Exchange.

Although the price of the acquisition was never officially announced, I understand it was close to €80 million and mostly in cash.

La Nevera Roja’s exit compared to Trovit and Akamon’s.

La Nevera Roja’s co-founders left the company after the deal was closed and they have now embarked on different projects. Iñigo Juantegui is about to launch a new startup and Jose del Barrio recently unveiled Samaipata Ventures, a €20 million venture fund focused on the ecommerce sector.

The acquisition took place at the right time for La Nevera Roja and its investors, who I understand also received offers from Just Eat and other food delivery companies before the deal was closed in February of last year.

At the time of the acquisition, Just Eat and La Nevera Roja had similar market shares in Spain. Just Eat has traditionally been a strong player in smaller Spanish cities, with La Nevera Roja being in a close second position in Madrid and Barcelona’s urban areas.

Since the acquisition took place, the differences between Just Eat and La Nevera Roja have widened, and nowadays Just Eat accounts for about 4 million annual deliveries while La Nevera Roja takes in about 2 million.

As a result of La Nevera Roja’s acquisition by Just Eat, the Spanish market will now be controlled by one single player, creating a monopoly in the local food delivery sector.

This is Just Eat’s third purchase in Spain, after it bought Sin Delantal in 2012 and Food2U in 2015. Evaristo Babé and Diego Ballesteros, founders of Sin Delantal, moved to Mexico after the deal, built Sin Delantal Mexico, and sold it again to Just Eat.

La Nevera Roja was acquired at its peak

Various sources close to the situation have told me that after the acquisition, Rocket Internet imposed strong limitations on the day-to-day operations of La Nevera Roja, which included cancelling the company’s well known TV advertisements and other features that accounted for a large portion of its sales. Significant changes in the company’s management team also took place.

“In a matter of weeks, sales fell dramatically and La Nevera Roja has never been able to recover itself. This is just the first step in Rocket’s strategy to sell many of the companies they acquired in January. The first steps in the company’s failed strategy of building a global food network”, an industry source who wishes to remain anonymous said.

I’ve reached out to Just Eat, Rocket Internet and La Nevera Roja and will update this article if I hear back from them.

Less than 12 months after it closed, Spain’s largest acquisition of 2015 is gone as Rocket Internet’s potential food empire tumbles.

El conocido agregador de noticias fundado por Ricardo Galli y Benjamí Villoslada en 2005 tiene nuevos dueños. Daniel Seijo, cofundador del grupo editorial Diariomotor y del fondo de inversión Civeta investments, y Domingo Remojón (Remo), director de iAsesoria, se han hecho con una participación “significativa” en uno de los portales con más tradición en la escena española.

La cuantía de la transacción no ha sido revelada por ninguna de las partes.

La entrada de Seijo y Remo en el accionario de Menéame supone un cambio importante en la dirección del agregador, que pasará a estar liderado por Dani Seijo como CEO. Remo se encargará de las labores de backoffice y de la gestión financiera del proyecto.

Seijo seguirá también al frente de los proyectos gallegos Diariomotor y de ‘¿Qué coche me compro?’ junto a su socio Oscar Miguel, “aunque centrado en la toma de decisiones más que en ejecución”.

Ricardo Galli, que desde 2005 estaba al frente del proyecto, dará un paso a un lado y, aunque seguirá ligado al proyecto como asesor y supervisor de las estrategias y desarrollos futuros, ya no formará parte de su gestión diaria. Galli, que también ha dejado su puesto como profesor del departamento de informática de la Universidad de las Islas Baleares, seguirá teniendo una pequeña participación en Menéame y comenzará una nueva etapa formando parte de un “gran proyecto en la empresa privada”.

Menéame comenzó su andadura en 2005 inspirándose en el portal americano Digg. La web permite a los usuarios enviar noticias que son votadas y comentadas por la comunidad, convirtiéndose en una fuente importante de tráfico para numerosos medios de comunicación de habla hispana.

El único accionista con el que ha contado la empresa desde su fundación es Martín Varsavsky, que en 2006 compró el 10% del capital de Menéame. Un año más tarde el fundador de Jazztel y Fon compró un 23% adicional, repartiéndose así a partes iguales el accionariado de la empresa.

La cuantía de la inversión o la valoración de Menéame en ambas transacciones nunca se hizo pública. Tanto Varsavsky como Villoslada continuarán teniendo una participación en Menéame.

El portal obtuvo el año pasado ingresos por valor de €100.000 y un pequeño beneficio. Con alrededor de siete millones de visitantes al mes, el nuevo grupo editorial que pasará a pilotar la nave naranja se presenta con dos objetivos: mantener las expectativas de los usuarios actuales del portal y construir un modelo de negocio que saque un mayor partido al tráfico recibido.

“Menéame nació para organizar las noticias mediante votación de los lectores y ese seguirá siendo su propósito”, afirman Seijo y Remo en declaraciones a Novobrief. “Sobre esa base, el reto está en adaptarla a las nuevas tendencias de consumo de contenidos, y encontrar un modelo de negocio que la haga sostenible y que sea compatible con lo que esperan los usuarios, fuertemente identificados con la plataforma.”

Preguntados por las cantidades de la operación, ambos indican que “lo importante no es lo pagado hoy, sino el nuevo impulso que va a tomar el proyecto a medio plazo, que esperamos le guste a toda la comunidad y consiga más y mejores cotas a todos los niveles.”

Además de la importancia de mantener la fidelidad de la comunidad actual de Menéame, Seijo y Remo consideran que la última Ley de Propiedad Intelectual y su tasa a los agregadores de noticias supone “un riesgo enorme porque encima de la mesa hay una ley que pone en peligro la viabilidad de la empresa”.

Sobre esta situación, comentan:

“No obstante, creemos que no se llegará a desarrollar porque es absurda, fue una pataleta de los medios en contra de Google y de rebote perjudica a Menéame. Está recurrida ante la Unión Europea porque no tiene sentido pagar por enlazar (otra cosa sería utilizar el contenido completo), y por nuestra parte haremos lo que esté en nuestras manos para defender Menéame ante esta ley. Además, los grandes grupos de medios de todo el mundo saben que su futuro pasa por adaptase y colaborar con los nuevos players, no en tratar de eliminarlos con leyes hechas a medida.”

Groupalia y Offerum, dos de las principales empresas del sector de los cupones y los descuentos online en España, se fusionaron en Marzo de 2015. Menos de un año después, la empresa resultante de la transacción está a punto de ser vendida a Ofertix, según varias fuentes cercanas al sector han confirmado a Novobrief.

El precio de la transacción no ha sido revelado.

Ofertix, también con sede en Barcelona y otro player en el sector de la agregación de descuentos online, fue fundada por Antonio Alcántara, uno de los cofundadores del portal de e-commerce Privalia.

Curiosamente, Lucas Carné y José Manuel Villanueva, los otros dos cofundadores de Privalia, fueron los principales impulsores de Groupalia en 2010.

Y por si la complejidad no fuese suficiente, Ofertix fue la empresa que estuvo a punto de hacerse con los servicios de Letsbonus el año pasado. La americana LivingSocial (comprada a su vez por Amazon), que había adquirido Letsbonus años atrás, alcanzó un principio de acuerdo con Ofertix que se rompió a última hora (algunas fuentes dicen que incluso en el mismo notario) y Letsbonus acabó volviendo a las manos de su por entonces equipo directivo.

Pero volvamos a Groupalia y Offerum un momento.

Groupalia fue durante años una de las tecnológicas españolas más capitalizadas del sector, habiendo conseguido en total más de 55 millones de fondos internacionales como Index Ventures (Typeform), Insight Venture Partners (Wallapop) o General Atlantic, además de clásicos patrios como Nauta Capital, Caixa Capital Risc y Atresmedia.

Estos tres últimos fondos fueron los responsables de la última ronda conocida de Groupalia, que dio salida a Index, Insight y General Atlantic sin plusvalías.

Offerum, fundada por Vicente Arias y Jesús Monleón en 2009, llegó a levantar más de dos millones de dólares de Cabiedes & Partners y Bonsai Venture Capital. Desde el verano, Monleón y Arias no participan ya en las actividades de la empresa fusionada.

La vida tras la fusión

Varias fuentes consultadas por Novobrief afirman que tras la fusión de Offerum y Groupalia, que dio lugar al grupo empresarial Merchant Digital Services, las tensiones fueron en aumento.

Albert Bosch, que dirigía por entonces Groupalia, abandonó el barco pocos meses después y se incorporó al mando Jorge Blasco. Bosch había entrado a trabajar en Groupalia en 2012 y recientemente ha fichado por Billy Mobile como CCO.

Bosch no fue el único en salir, sino que también lo hicieron muchos otros trabajadores que se habían incorporado a Merchant Digital Services desde Offerum. Además, la tecnología aportada por esta última empresa fue descartada por la nueva dirección.

Desde entonces, afirman numerosas fuentes, el grupo ha centrado sus esfuerzos en la expansión de Bellahora, el marketplace de salones de belleza lanzado por Offerum hace aproximadamente dos años.

Offerum y Groupalia, que seguían facturando cifras respetables pero lejos de sus cotas más altas, pasan a mejor vida. Como una fuente anónima apuntaba en relación a la operación: “El negocio da dinero, pero también puede dar problemas en el futuro y nadie duda de que el sector de los cupones tiende a la baja”.

Novobrief se ha puesto en contacto con las diferentes partes por si hubiese algún comentario oficial al respecto.

La Nevera Roja ha dado mucho que hablar en España en el último año. La empresa fundada por Íñigo Juantegui y José del Barrio fue comprada por Rocket Internet en Febrero del año pasado por 80 millones de euros.

Exactamente un año después, y como adelantó Novobrief a finales de febrero, la startup de comida a domicilio fue vendida de nuevo, pasando esta vez a manos de Just Eat como parte de una operación que afectaba también a otros negocios de Rocket en Italia, México o Brasil. La compra de las cuatro empresas se cerró en €125 millones.

A raíz de la noticia, numerosos medios, inversores y analistas españoles aprovecharon la ocasión para clamar a los cuatro vientos que la operación que Rocket había hecho con La Nevera Roja era ruinosa y que, la venta original, había sido un “pelotazo” por parte de los fundadores e inversores originales de la compañía.

La mayoría de análisis tenían como base un supuesto mal comportamiento de La Nevera Roja tras la compra de Rocket. Novobrief se equivocó también en ese aspecto. Estas teorías fueron rápidamente desmentidas por el actual CEO de la compañía, Íñigo Amoribieta, que afirmó que el año 2015 había sido uno de los mejores en la historia de LNR con un incremento del 100% en pedidos (con respecto al año anterior) y un +241% en ingresos.

Rocket Internet en ningún momento explicó qué parte de esos €125 millones de euros pagados por Just Eat correspondían a cada uno de los cuatro negocios vendidos.

Jesús Martínez, en El Español, publicó al poco tiempo de hacerse oficial la noticia que el precio de LNR “representaría la mayoría de esa factura pagada por Just Eat”.

El Confidencial, sin embargo, afirmó que “La Nevera Roja ni siquiera representa el 25% del valor de la operación total, ya que supone un mercado visiblemente inferior al mexicano y, sobre todo, al brasileño”.

Nada más lejos de la realidad

Según ha podido saber Novobrief, las cifras en las que se cerró la operación se asemejan mucho a las publicadas por El Español en su momento.

Fuentes cercanas a ambas compañías afirman que Just Eat pagó €76 millones a Rocket Internet por La Nevera Roja (el 60% del total), €36.7 por el negocio en Italia, €6.5 por el brasileño y alrededor de €5.8 millones por la parte mexicana.

La Nevera Roja se habría revendido así por casi lo mismo que Rocket Internet pagó originalmente por la compañía.

El acuerdo, dicho sea de paso, está pendiente de la aprobación por parte de la Comisión Nacional de la Competencia.

Kibo Ventures is about to launch a new fund. If all goes according to plan, the fund will be almost double the size of the first one (€80 million vs. €45 million), allowing the firm to lead or co-lead investments in the €2 to €5 million range.

Not a lot of investment firms can reach that level in Spain at the moment, and with so much seed capital available for startups, the firm led by Aquilino Peña, Javier Torremocha and José María Amusátegui believes they can make a difference at the Series A and B stage.

To know more about the firm’s intentions, the differences between the new and old fund and LPs’ appetite for technology companies, we sat down with Aquilino Peña for a short interview.

You’ve significantly increased the size of this new fund, from €45 to €80 million. What’s going to change with it? Is Kibo’s focus different this time?

The focus is the same as before: to invest in digital companies. We don’t invest in hardware, retail, consumer electronics or in other capital-intensive sectors that require large sums of money to launch a product or service. In digital we’ve made deals in all kinds of sectors, mostly because the Spanish market doesn’t allow you, as an investor, to focus on a niche or single sector.

We’re big fans of transactional models (SaaS, ecommerce enablers, marketplaces), mobile and companies with a strong tech component.

Can you find enough projects in Spain to justify spending €80 million in them? In other words, are you going to continue to invest only in Spanish companies or are you also looking at other countries and regions?

One third of the 31 companies in our portfolio are in the US, so we don’t only look at Spain-based companies. That said, the common trait in our portfolio is that there’s always a Spanish connection: the founding team, the development team, etc.

We do make deals outside of Spain under that thesis, but only when we can contribute to their success in some way and when there’s a Spanish link in them. Many of the companies we have backed have launched in the US with our support, and we like to help in any way we can.

You’ve always said that, with so much capital at the seed stage in Spain, there’s a big opportunity for firms investing in large Series A and B rounds. Is that Kibo’s goal with this new €80 million fund?

Our average investment in our current fund is €1 million. With the new one, we want to invest in fewer companies but with the capability of deploying more capital than before in each of them, between €3 and €4 million per company.

With the new fund we’ll have the same entry point, but we want to be able to lead or co-lead €2 to €5 million rounds in Spanish companies. Right now it’s very tough for startups to find local money at that stage and the fundraising process tends to be an even bigger distraction for teams.

We’re hands-on investors, we believe we know very well our companies and that’s why we want to lead those type of deals, instead of just making small follow-on investments.

VCs don’t talk much about their own investors. Who is backing Kibo this time? Are Telefonica with Amérigo or Mutua Madrileña investing once again?

We’re right in the middle of the fundraising process and all LPs from our first fund have encouraged us to launch the second one, and they have backed us. Pretty much every single one of them have already committed capital to the new fund, and those that have not, are currently discussing it internally. Our objetive is that all of our previous investors join us once again, and it’s looking good.

We’re very happy with Telefonica’s Amerigo, and we collaborate with the company at all levels: sales agreements, co-investments, analysis of opportunities and support in their various entrepreneurship programs under the Open Future umbrella.

There are a lot of funds raising capital at the moment. I think LPs are very selective when it comes to backing VCs, and not every single fund currently fundraising will be able to reach their goals. You need to have experience, strong differentiating factors and a strategy and focus that you can explain well.

In our case, we have all of that and we also have the support of our previous LPs. The process is going very well for us.

People often talk about how tough it is for a startup to raise funding. But, what’s the process like for a fund like Kibo? Is there a lot of interest from LPs to get into the technology market?

The problem we have in Spain is that the number of institutional investors willing to invest in Venture Capital is very limited. That’s one of the reasons why companies like Telefonica or public entities such as FondICO or CDTI’s Innvierte play such a vital role in the sector.

“In Spain the number of institutional investors willing to invest in Venture Capital is very limited” – Aquilino Peña

This problem is slowly but surely being solved, mostly thanks to companies that are performing well and growing, coupled with significant exits and low interest rates.

What many LPs and institutional investors now realise is that they’re better off investing in Venture Capital firms with strong track records than investing that capital themselves.

You told me that the new fund will have a size of between €60 to €80 million. Does its final size depend on how much public money you’re able to get?

We’re the only fund in Spain that, so far, has received support from FondICO and CDTI in both of our funds, the old one and the new one.

We’re also in talks with the EIF (European Investment Fund), which is the largest institutional investor in the European Venture Capital scene, managed by people with a lot of experience in the sector. We’ll be happy to have them on board, but they’re not investors yet.

What are you most proud of in your first fund?

One of the key advantages of our portfolio is that we don’t depend on one or two companies to perform well. We’ve been able to build a portfolio that has seen very few casualties.

We’ve invested in 31 companies, we’ve sold profitably three of those, four have shut down (less than 5% of all) and two more are currently struggling.

All in all, we have a very solid and growing portfolio, with aggregate annual sales of €50 million and with more than 800 employees. These are companies that have found their market and have real clients. Thanks to our efforts to stay connected in the ecosystem, we’ve been able to invest in some of the better companies in Spain today. Some of the most valuable in our portfolio are Flywire (peerTransfer), CartoDB, Redbooth or Jobandtalent; but we’re also investors in others that have great potential, Captio, iContainers, Custodio or MediaSmart.

These days, on the consumer side, it seems as if two main kind of apps are the most lucrative: games and dating applications. If you take a look at the top grossing apps on iOS or Android’s app stores, you’ll see a wide variety of the latter, from Tinder to Happn. Groopify wants to get there.

The Madrid-based startup is not just a dating app, but also a platform that makes it easier for groups of young people who don’t know each other to meet up for a drink. Like a blind date, but more sophisticated and with more people involved.

According to Pablo Viguera, co-founder and CEO, in 18 months the app has more than 100,000 registered users and the number of businesses that have partnered with the app has surpassed the thousand mark.

As Groopify brings new customers to bars and cafés, the company believes it can monetise that relationship to build a sustainable business model.

“We don’t only provide recurrent and quality traffic to bars thanks to our meetings, but we also help them in their communication and marketing efforts”, the company says. Groopify charges a pay per lead commission to bars. The company is not publicly saying how well that business model is working, nor will it disclose sales or revenue figures.

Viguera did say in a statement that in the last 12 months the number of plans created by users has grown 10X, and that 2,000 plans are created on a monthly basis in 45 different Spanish cities.

To expand its presence and start rolling Groopify internationally, the startup has just closed a €800,000 round of funding led by media for equity investment firm Media Digital Ventures (Atresmedia, Godó, Vocento), Pinama Inversiones and business angel José María Torroja (through a Startupxplore syndicate).

Groopify had previously raised €180,000 from Plug and Play Spain, Grupo Zriser, Civeta and Carlos Domingo.

Example of the 8 Spanish entrepreneurs educated at MIT and global leaders in their fields.

This guest post was written by Iñaki Berenguer, currently the founder & CEO of CoverWallet. Prior to that, Iñaki founded and led Contactive and Pixable (both acquired), and worked at McKinsey, Microsoft and HP.

This summer, Nobel prize winnerPaul Krugman published anarticle in the New York Times about the dominance of MIT trained economists in global policy positions. He gave as examples, apart from himself,Ben Bernanke,Mario Draghi,Olivier Blanchard orMaurice Obstfeld, Chief Economists of the IMF, European Central Bank, or Federal Reserve. Morerecently, a new ranking puts MIT as the top ranked university worldwide. And this very week, MIT published astudy about the impact of the university in the creation of businesses, that in turn generate employment for 5 million people and enough income to be ranked as the 10th largest economy in the world in terms of GDP.

It’s very remarkable that a university that accepts only 1,100 students in its freshmen class has graduates with that level of impact. Not only in Economic Policies, but also with the global establishment, with individuals likeBenjamin Netanyahu,Carly Fiorina,Kofi Annan,John S. Reed (President of Citigroup), orWilliam Clay Ford (CEO of Ford), as well as in the creation of technology companies like Dropbox, Texas Instruments, Intel, HP, Analog Devices, Akamai, Qualcomm, Bose, Genentech and Koch, 80 Nobel prizes (Spain has only 8), and visionaries such asSir Tim Berners Lee orNoam Chomsky.

MIT and the Spanish startup ecosystem

But the really remarkable thing is the impact of MIT in Spain. For example, less than 10 students each year get accepted into MIT Sloan. Even so, this has an interminable representation in the Spanish establishment. Some of those who graduated MIT includeCarlos Torres (President of BBVA),Rafael del Pino (President of Ferrovial),Tomás Pascual(President of Leche Pascual), Matías Rodríguez Iniciarte (Vice Chairman of Santander Bank),Joaquin Moya (President of IBM Spain),Miguel Milano (President of Oracle Spain and Salesforce),Enrique Casanueva (President of JPMorgan Spain), Nuria Oliver (Scientific Director of Telefonica),Fernando Perez-Hickman (Chairman Sabadell Bank), orMaria Teresa Pulido (Board member of Bankinter), as well as a number of partners at McKinsey, BCG, Bain or ATKearney.

But I wanted to talk about the impact of MIT in Spain, and specifically, in the innovation and creation of startups with global impact. I’ve chosen 8 prominent examples of Spanish entrepreneurs educated at MIT (just like me) whose startups are worldwide referents in their fields:

Iker Marcaide, founder of peerTransfer (Flywire) in 2009, world leader in international payments. The startup has received more than $40 million in funding from investors like Bain Capital o Accel (Facebook investors), and has processed transactions worth of +$2bn.

Jose Mariano López Urdiales, founder of Bloostar, a pioneer company in the launching of nanosatellites. Also included in his team isMichael Lopez-Alegría, a Spanish astronaut that maintains NASA’s world record for most days in space.Here you have a video of their launch.

Bernat Ollé, founder of PureTech Ventures and founder of Vedanta Biosciences, that develops pharmaceuticals from bacteria and that recently signed a $250MM agreement with Johnson&Johnson.

Javier García Martínez, founder of Rive Technology, which develops nanomaterials to maximize the performance of catalyzers used in the refining of oil and has received $80 million in funding.

Angel Diaz Alegre, founder of iDoctus, a tool of mHealth for doctors.

In the last few years, many groups of Spanish tech innovators are emerging with global ambition (apart from the ones mentioned, there are many more like JobandTalent, Wallapop, Ticketbis, Typeform, CartoDB or AlienVault) that have become global referents in their industries, something that was unthinkable 10 years ago.

A decade ago, the path was to grow first in Spain and after a number of years, get out into the world, which in the majority of cases did not end up happening. This is changing and the representation of MIT for this type of global founders is really formidable.

The MIT gang

What distinguishes MIT and what makes it so innovative? Its DNA and the entrepreneurial culture.

MIT was created almost two centuries ago with the motto “Mens et manus” (Mind and Hand) to give technological service to the needs of the industrial era. And as the world was changing at a dizzying speed, in recent years MIT has also transformed into an incubator of leaders in the digital era. Leaders that are prepared to face the challenges of modern society and take advantage of opportunities that this changing world presents with the support of new technologies.

“For innovation-driven startups, the ability to enter and potentially disrupt a market requires not only innovative ideas, but also productive workers to commercialize and execute those ideas”, Professor Ed Roberts.

The whole university breathes the passion to innovate, and its DNA, coupled with its capacity to bring together the most brilliant minds on the planet, becomes an explosive combination.

This, when added to an ecosystem of investors, advisors, professors that have founded companies, mentors, funding, coworking spaces, state-of-the-art research, a multitude of classes about entrepreneurship, offices of assistance for those starting out, labs of large technological companies (e.g., Microsoft, Google, Facebook, etc) located in the same campus, and daily networking opportunities, prepares you to create companies that change the world using new technologies.

I started Novobrief because I thought, and I still do, that the Spanish startup ecosystem could be covered in a better way and because I believed investors, entrepreneurs, corporates and the general public outside of Spain should know what was going on in the country.

The idea behind the project was always to build a business that could support myself, but I haven’t been able to achieve that and, in the process, I’ve also learned that simply covering Spain is too low of a ceiling.

A few months ago I started working on a database of Spanish startups with Javier Escribano. We both believed that building a database of such characteristics could be useful for local startups, entrepreneurs and investors. And also, it could represent a new source of income for myself and the blog.

Also around then, I had another conversation with Robin Wauters, whom I have known and respected for many years. We talked about what he had in mind for Tech.eu and it all sounded very familiar with the way I saw things for the future of Novobrief, but with Europe (and not just Spain) as a starting point.

Several conversations later, we agreed that I’d join Tech.eu as a data analyst/journalist. I’m starting this week.

I’m super excited about the opportunity and what I’ll be doing in the near future. I won’t be publicly publishing a lot of stories anymore, but I’m sure I’ll learn ten times as much.

Novobrief won’t go away and nor will the newsletter.

It’s taken me a lot of time and hard effort to build this, and I don’t want it to disappear. Obviously, I won’t be publishing as much as before and this will become more of a personal publication focused on the Spanish startup scene. But I will continue to do so from time to time, and I might even publish a few articles in Spanish.

Por primera vez en la historia de España, en 2015 se invirtieron más de 500 millones de euros en empresas tecnológicas españolas. Lo que viene a ser en la mitología estartapil, un medio unicornio.

Sin más datos en la mano, es difícil afirmar que 2015 ha sido un año record en otros aspectos del panorama patrio de startups. Sin embargo, y ayudado en mi mala memoria, creo que no me cojo los dedos si digo que el año pasado fue también especialmente bueno para los inversores españoles.

No porque se invirtiera más dinero que nunca en empresas españolas, sino porque los propios fondos de capital riesgo locales y otras sociedades de inversión levantaron cantidades ingentes de capital que ahora tendrán que determinar en qué empresas meter.

Mientras que en 2014 los tres principales fondos de inversión que se cerraron fueron los de Axon, Caixa Capital Risc y Cabiedes & Partners, sumando casi 100 millones de euros, en 2015 la lista es mucho mayor.

Qualitas anunció a mediados de año un fondo de 60 millones para invertir en etapas maduras. Después de años de sequía, Nauta Capital hizo lo mismo y parece que van encaminados a cerrar su nuevo fondo en 150 millones de euros. Hotusa Ventures hizo lo propio con un vehículo especializado en el sector del turismo. Carlos Blanco parece que va a montar un fondo de early stage de 20 millones. Dice la leyenda que Javier Santiso está a vueltas con el suyo de growth, pero que le está costando más de lo previsto cerrarlo. Lánzame Capital prepara 20 millones para principios de este año, elevando su anterior pledge fund a la enésima potencia. Samaipata Ventures apareció a finales de 2015 con 20 millones bajo el brazo para empresas de ecommerce, apoyados en la multimillonaria venta de La Nevera Roja. Kibo Ventures cerró el año afirmando que Papá Noel ha bajado este año por la chimenea con un cheque de 80 millones. Galdana Ventures tiene 150 millones en la saca para invertir en otros fondos. Y, esto todo, sin contar con el nuevo fondo que K Fund (Vitamina K, Iñaki Arrola) espera cerrar pronto y que andará entre los 40 y los 50 millones.

En total, y si se confirman los que quedan por cerrar, hablamos de en torno a 550 millones de euros que están esperando ser invertidos en empresas tecnológicas.

Por poner estas cifras de fundraising en contexto: entre 2015 y los primeros meses de 2016 es muy probable que el dinero levantado por los fondos… sea superior al invertido en todo 2015. Y 2015 fue un año record.

O dicho de otra forma, entre 10 y 15 fondos de capital riesgo españoles tienen en sus manos una cantidad de dinero lista para ser invertida… superior a la suma de todo lo invertido en 2013 y 2014 (221 y 285 millones, respectivamente).

Resulta un tanto curioso que después, algunos fondos, se echen las manos a la cabeza con las valoraciones de algunas startups early stage. ¡Burbuja! No recuerdo muchas cosas de la carrera, pero sí recuerdo que una de las primeras cosas que te enseñan en macroeconomía es que a mayor cantidad de dinero en circulación en el mercado, mayores precios.

El ‘montemos una startup, que está de moda’ parece que se ha convertido este año en el ‘montemos un fondo, que hay pasta de sobra’. Y hay mucho dinero por dos principales motivos: porque el Estado, a través del ICO, está subvencionando el sector con 1.500 millones de euros para los fondos y porque mucho inversor no tecnológico se está acercando a la tecnología como un niño se acerca al mando de la Play el día de Reyes.

Visto el panorama cabe preguntarse en dónde se va a invertir todo este dinero.

Según las cifras que he ido recogiendo para Novobrief estos últimos años, de 2013 a 2015 la cantidad invertida en startups españolas se incrementó un 142%. Sin embargo, el número de operaciones (dicho de otra forma, la cantidad de startups listas para recibir inversión), tan solo un 23%.

Con más cantidad de dinero disponible que nunca en el mercado, ¿a dónde va a ir a parar? Uno podría pensar que los fondos españoles comenzarán a invertir fuera de España, pero más allá de Nauta Capital, Axon, Active VP y Seaya Ventures, pocos lo han hecho en los últimos años. En parte, me imagino, porque el deal-flow de mucho inversor español más allá de nuestras fronteras es tan bueno como la calidad del aire de Madrid.

Cabiedes & Partners, un clásico de la inversión patria, decía en 2014 que con el nuevo fondo comenzarían a invertir fuera de España. Como se suele decir en interné, ‘photo or didn’t happen’, y por ahora parece que es más lo segundo.

Todo esto, sobre todo la (no) exposición internacional de los fondos españoles, ocurre en un momento en el que cada vez más fondos de UK, Francia o Alemania nacen con un enfoque pan-europeo desde el día uno.

Si el mercado objetivo para la mayoría de fondos españoles empieza en Tarifa y acaba en los Pirineos. ¿A dónde carallo van a ir a parar todos esos millones de euros que están esperando para ser invertidos?

Today was the official unveiling of the 2016 edition of 4YFN, one of the leading startup and technology events in Spain. Organised by Mobile World Capital, the conference will take place in Barcelona from February 22 to 25 and will bring together 12,000 attendees, 500 investors and startups from all over Europe.

For this year’s edition, MWC asked me to put together a report on the Spanish startup ecosystem, which you can see embedded above. The report was presented by MWC’s CEO Aleix Valls.

Disclaimer: this was paid work.

I think it’s a pretty good summary of what happened in Spain in 2015 and the main challenges the country still faces when it comes to building technology companies. One thing that I forgot to include in the report is the fact that in 2015 Spanish VC firms raised almost more capital than what was actually invested, which makes you wonder where all that money is going to go (over the next few years) and which will increase investor competition and push valuations higher.

PS: If you want a higher quality (images & graphs) version of the report, get in touch (jaime@novobrief.com) and I will send you one.

Just Eat is going to get its hands on the company once founded by Jose del Barrio and Iñigo Juantegui, becoming a de facto monopoly in the Spanish delivery industry with approximately 6 million annual deliveries.

While I understand that the transaction between Just Eat and Rocket Internet will be closed soon, the Berlin-based giant is waiting to complete the sale of other business units in its Global Online Takeaway Group to make an official announcement.

Global Online Takeaway Group is the name of the holding company Rocket created in February of last year when it acquired at least 7 food delivery companies in two different continents, including La Nevera Roja and Pizzabo (Italy). At the time, Rocket also announced a €496 million investment in Delivery Hero, one of the bigger companies in the sector and a competitor of FoodPanda.

Since its IPO in October 2014, Rocket’s stock price has dropped by more than 50% and currently trades at €18.80. At the time of the IPO, the German giant had a market cap of €8.4 billion. Rocket’s current market cap stands at €3.10 billion, still the most valued technology company in Europe.

Rocket has come under strong scrutiny by investors and the media in recent times. According to Reuters, the company decided at the last minute to put HelloFresh’s IPO plans on ice due to internal turmoil and significant differences with Kinnekiv, the Swedish investor firm that controls 14% of Rocket’s shares and is also a major investor in many of its subsidiaries.

On the other hand, UK-based Just Eat’s share price rose 40% over the past 12 months while orders increased by 57%.

In October 2015, the Financial Times wrote about “the German ecommerce group struggle for profitability”, citing numerous analysts and investors who have, for a long time, complained about Rocket Internet’s complexity. Rocket has lost a number of key senior managers over the past few months.

Co-founder Oliver Samwer talked about these and other issues at London TechCrunch Disrupt in an interview on stage.

According to my sources, Rocket is also planning significant layoffs at Linio, one of the largest online retail stores in Latin America. These sources say that 30% of Linio’s staff could be let go in the next few weeks. Linio currently has 1,500 employees across the region.

A 12-month acquisition

La Nevera Roja’s acquisition by Rocket Internet was the largest exit by a Spanish technology company in 2015, not counting Mitula’s IPO on the Australian Stock Exchange.

Although the price of the acquisition was never officially announced, I understand it was close to €80 million and mostly in cash.

La Nevera Roja’s exit compared to Trovit and Akamon’s.

La Nevera Roja’s co-founders left the company after the deal was closed and they have now embarked on different projects. Iñigo Juantegui is about to launch a new startup and Jose del Barrio recently unveiled Samaipata Ventures, a €20 million venture fund focused on the ecommerce sector.

The acquisition took place at the right time for La Nevera Roja and its investors, who I understand also received offers from Just Eat and other food delivery companies before the deal was closed in February of last year.

At the time of the acquisition, Just Eat and La Nevera Roja had similar market shares in Spain. Just Eat has traditionally been a strong player in smaller Spanish cities, with La Nevera Roja being in a close second position in Madrid and Barcelona’s urban areas.

Since the acquisition took place, the differences between Just Eat and La Nevera Roja have widened, and nowadays Just Eat accounts for about 4 million annual deliveries while La Nevera Roja takes in about 2 million.

As a result of La Nevera Roja’s acquisition by Just Eat, the Spanish market will now be controlled by one single player, creating a monopoly in the local food delivery sector.

This is Just Eat’s third purchase in Spain, after it bought Sin Delantal in 2012 and Food2U in 2015. Evaristo Babé and Diego Ballesteros, founders of Sin Delantal, moved to Mexico after the deal, built Sin Delantal Mexico, and sold it again to Just Eat.

La Nevera Roja was acquired at its peak

Various sources close to the situation have told me that after the acquisition, Rocket Internet imposed strong limitations on the day-to-day operations of La Nevera Roja, which included cancelling the company’s well known TV advertisements and other features that accounted for a large portion of its sales. Significant changes in the company’s management team also took place.

“In a matter of weeks, sales fell dramatically and La Nevera Roja has never been able to recover itself. This is just the first step in Rocket’s strategy to sell many of the companies they acquired in January. The first steps in the company’s failed strategy of building a global food network”, an industry source who wishes to remain anonymous said.

I’ve reached out to Just Eat, Rocket Internet and La Nevera Roja and will update this article if I hear back from them.

Less than 12 months after it closed, Spain’s largest acquisition of 2015 might be soon gone gone as Rocket Internet’s potential food empire tumbles.

UPDATE:

La Nevera Roja’s CEO, Iñigo Amoribieta provided this statement to our friends at Hipertextual. In it, the company does not confirm nor deny what Novobrief has published:

“Since I joined La Nevera Roja, there have been acquisition rumours from various companies. As anyone can imagine, La Nevera Roja would represent a strategic acquisition for Just Eat, given our strong position in Spain, and for other players in the sector that would want to have a presence in Spain.

Contrary to what the article says, the author never got in touch with us and, La Nevera Roja, far from suffering a deceleration in its sales over the past few months, has been breaking records in orders, revenue and margins. This seems like a way, using the press, to destabilise a competitor o decrease the price of, as we’re saying, what could be a strategic acquisition.

For now, we don’t have anything else to add.”

On December 26 2015 I did ask LNR’s CEO about the possibility of the company ceasing its operations, which is what the first rumours I heard said. This morning, minutes before the publication of this story, I sent three emails to La Nevera Roja, Rocket Internet and Just Eat to get their side of the story. In full honesty, I probably should have done it earlier than that.

UPDATE #2:

La Nevera Roja has sent me a new statement, denying that the sale has been completed:

“Like any great and strategic business, La Nevera Roja has been approached at various times by parties for a corporate transaction, but there has been no sale of La Nevera Roja. La Nevera Roja has continuously broken records in orders, revenues and margins through 2015, a trend which continues into 2016.”

UPDATE #3:

Rocket Internet has confirmed the news. The German company has sold its food delivery subsidiaries in Mexico, Brazil, Italy and Spain for €125 million.

“The transaction is in line with Rocket Internet’s strategy to divest non-core operations that are not market-leading. The sale of La Nevera Roja and PizzaBo further reduces the complexity of Rocket Internet. The LPV including cash remains at the latest disclosed figure of €7.2billion as of 30 November 2015.

(…)

It is anticipated that the transaction in Spain will be completed by the end of Q2 2016, as it is still subject to regulatory approval from the Spanish competition authority, the Comisión Nacional de los Mercados y la Competencia.”